Bitcoin Correlation Analysis: Relationships Remain Spurious

Bitcoin's correlations with the S&P 500, Gold, and the USD remain spurious and largely unexplained

Contents

A Prelim

My Model Outputs: Pearson, Spearman, Conditional Beta, and Copula

Qualitative Overlay

Links To My Models + The Academic Studies Mentioned In #1

NB: Disclaimer

This piece communicates a brief correlation analysis, where I tested Bitcoin’s correlation with the S&P 500 (SPY 0.00%↑), Gold (GLD 0.00%↑), and the USD Index – Links to all academic papers and model code are enclosed at the tail end of the article.

1) A Prelim

Studies surrounding BTC’s correlation to major asset classes vary in findings, largely due to variation in depth and periodicity. In a recent study, Tsuji (2023), regressed Bitcoin’s daily returns between January 2, 2020 and November 29, 2022, discovering a linear correlation coefficient of 0.403 and an adjusted R-squared of 16.1%. In contrast, Jiang et al. (2022) studied daily returns between 2015 and 2020, finding an adjusted R-Squared of 0.6592. The latter’s results contradict Tsuji’s, possibly due to regime change, sampling periods, and/or methodological discrepancies; however, that’s just me speculating…

To my observation, financial institutions tend to publish superficial correlation analysis and rarely describe their correlation outputs. In this analysis, I aim to bridge the gap between Tsuji (2023) and Jiang et al. (2022) by testing a longer horizon, ranging from January 2015 -July 2025. Moreover, I opted for a monthly regression as opposed to a daily periodicity.

Aside: This is a light paper, it’s not peer reviewed, and shouldn’t be considered as such.

2) Model Outputs

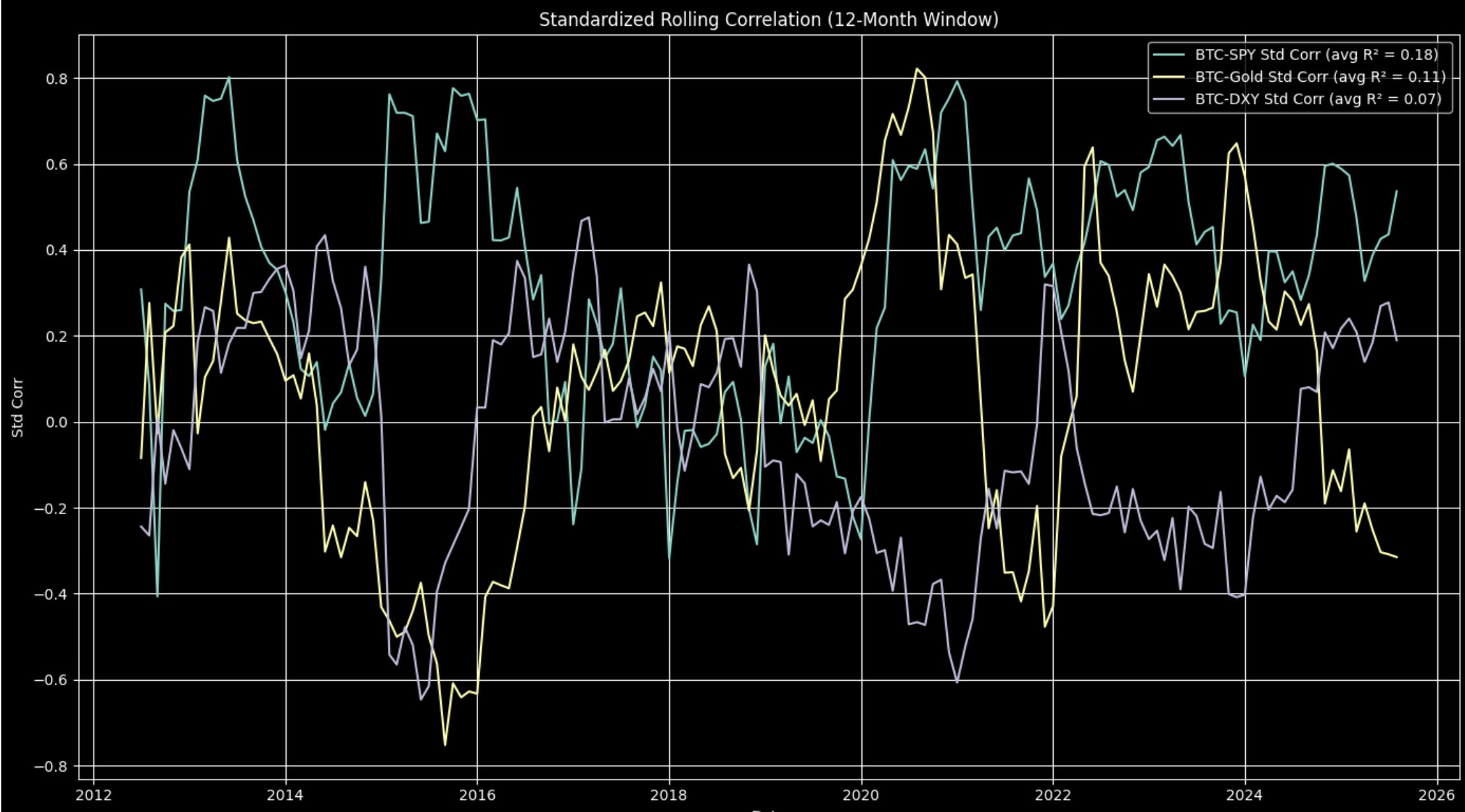

Pearson Correlation

Pearson correlation measures linear correlation, which is quite redundant for BTC due to the asset’s volatility. That said, I decided to use Pearson as a base, where I standardised the variables to adjust for outliers – Bitcoin’s correlation results are spurious. Moreover, docile R-Squared values suggest BTC’s explanatory variables remain adrift from those of the S&P 500, Gold, and the USD Index. Correlations may increase during stressed periods or trending markets, but under normal conditions, BTC’s influencers remain distinct from those of other major asset classes.

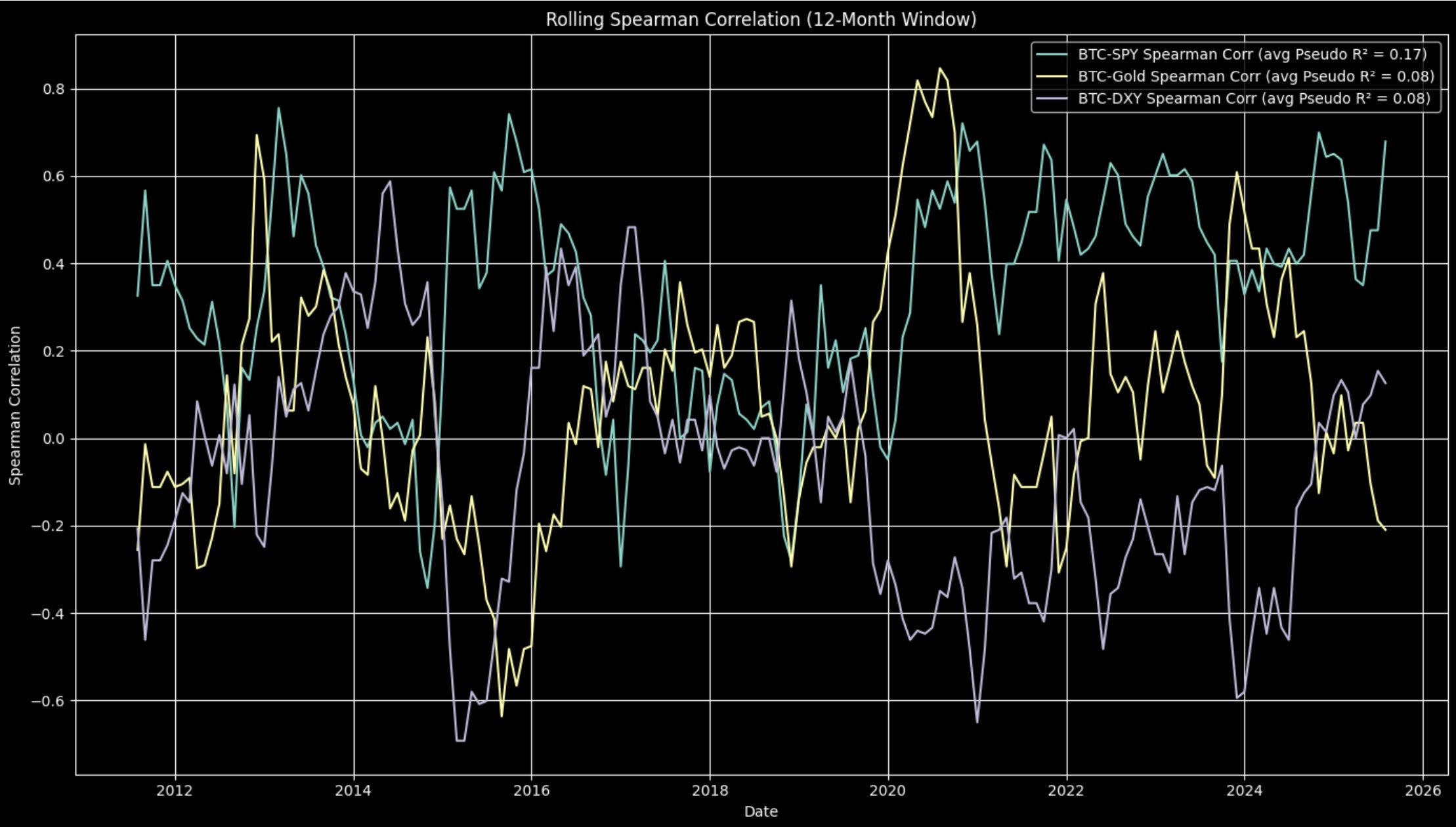

Spearman Rank

Though linear, Spearman ranks correlations, providing researchers with a heuristic idea of non-linear correlations. Similar to Pearson, my Spearman test suggests BTC’s correlations with other major asset classes remains spurious and largely unexplained.

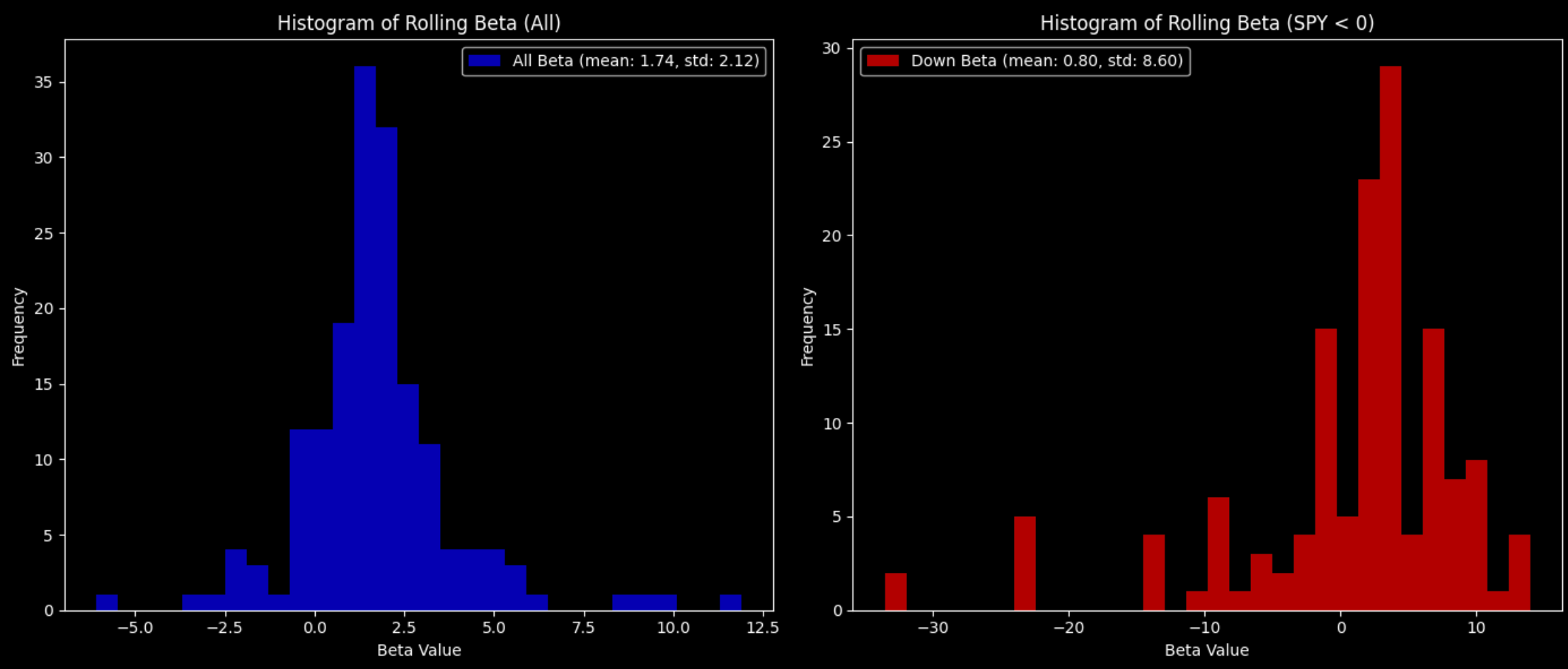

Conditional Betas

A beta coefficient is written as follows:

Beta = Correlation Coefficient * [Standard Deviation of Asset A / Standard Deviation of Asset B]

I conditioned Bitcoin’s beta relative to the $SPY, where I accounted for median beta and down market beta. As illustrated in the following figure, the throughout-the-cycle beta coefficient dominates the down market beta coefficient – I find this quite interesting as it illustrates that BTC shares excess upside slope sensitivity than downside slope sensitivity. In other words, its tail risk is somewhat idiosyncratic from the S&P 500’s tail risk.

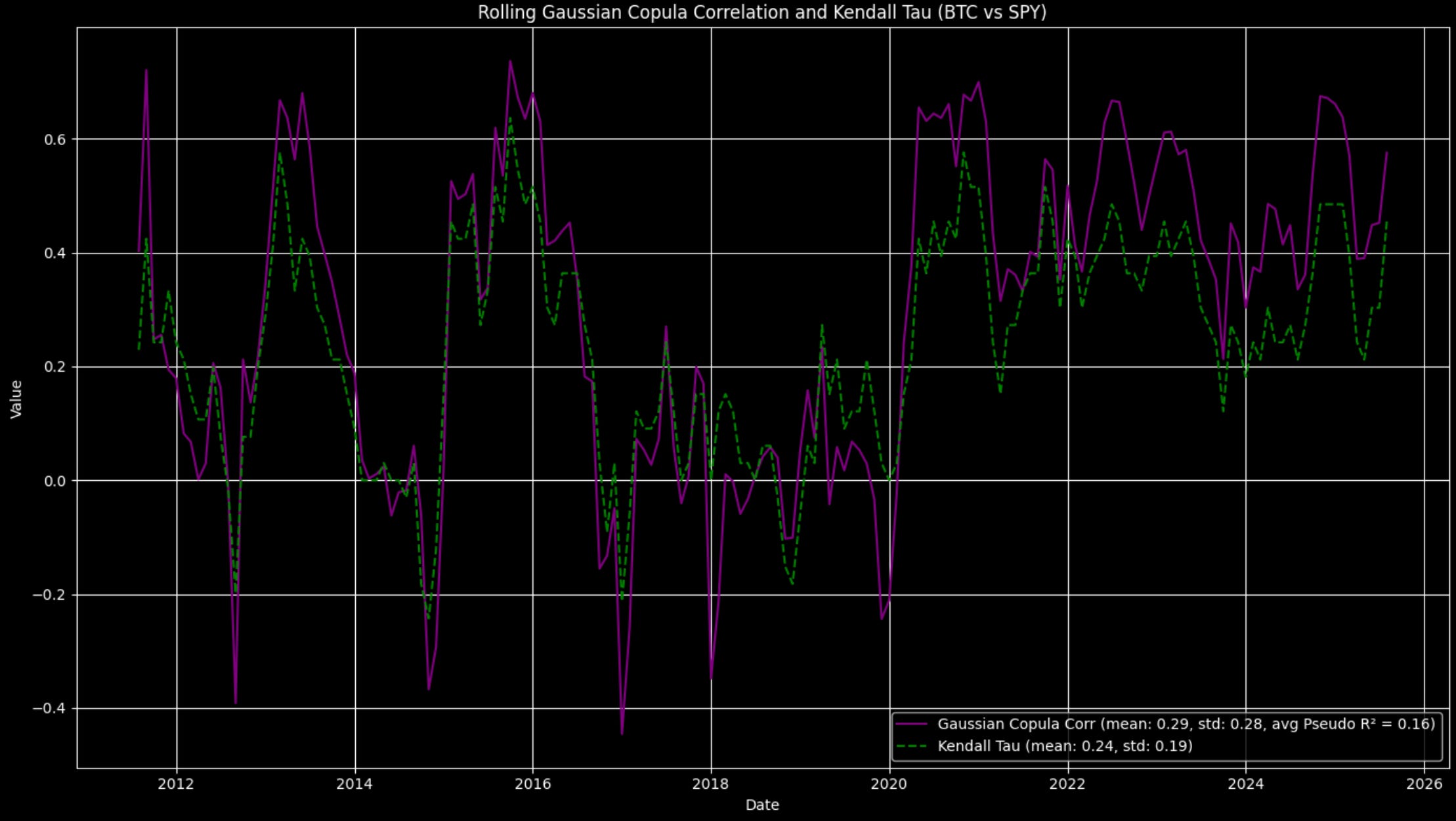

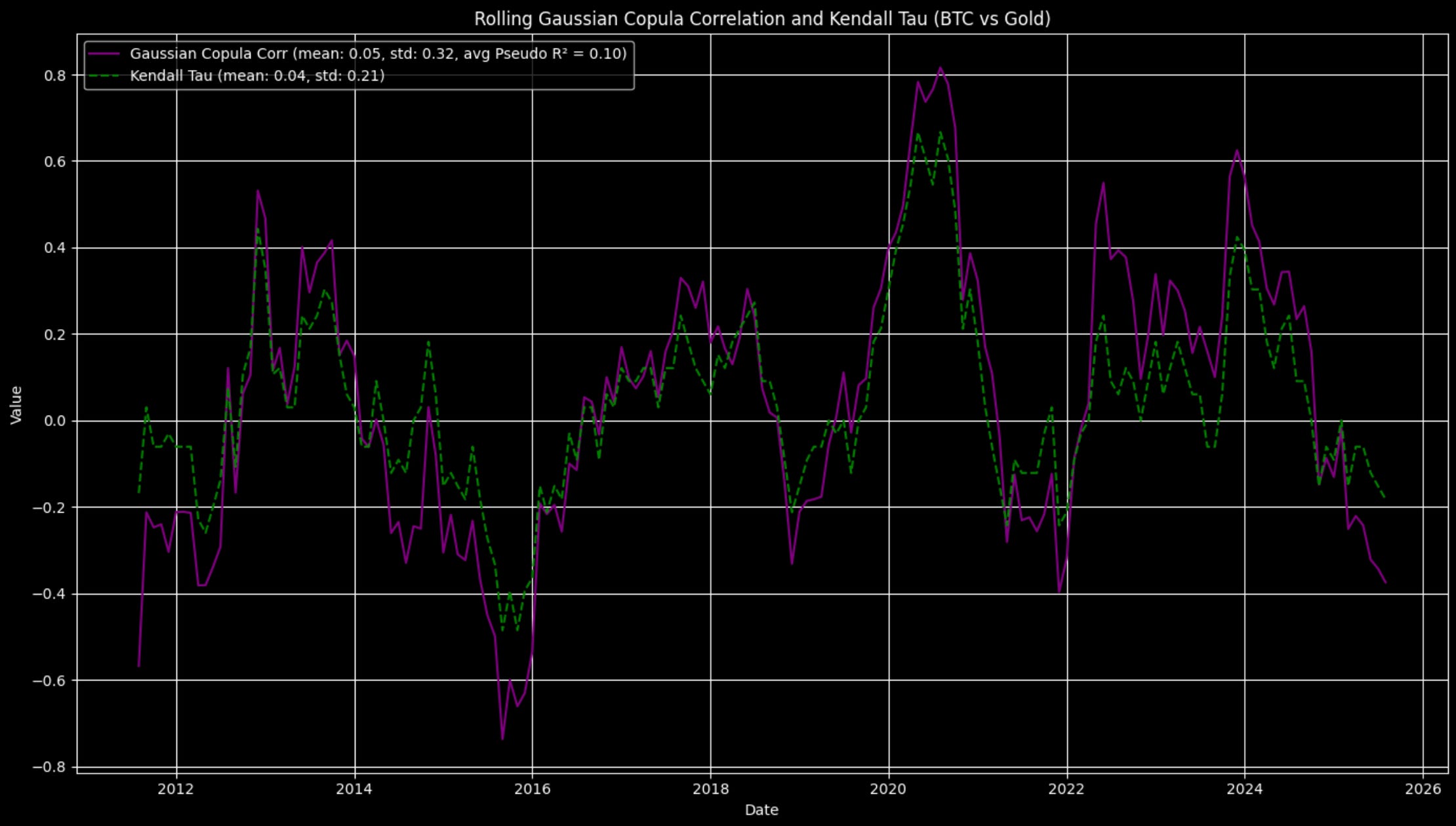

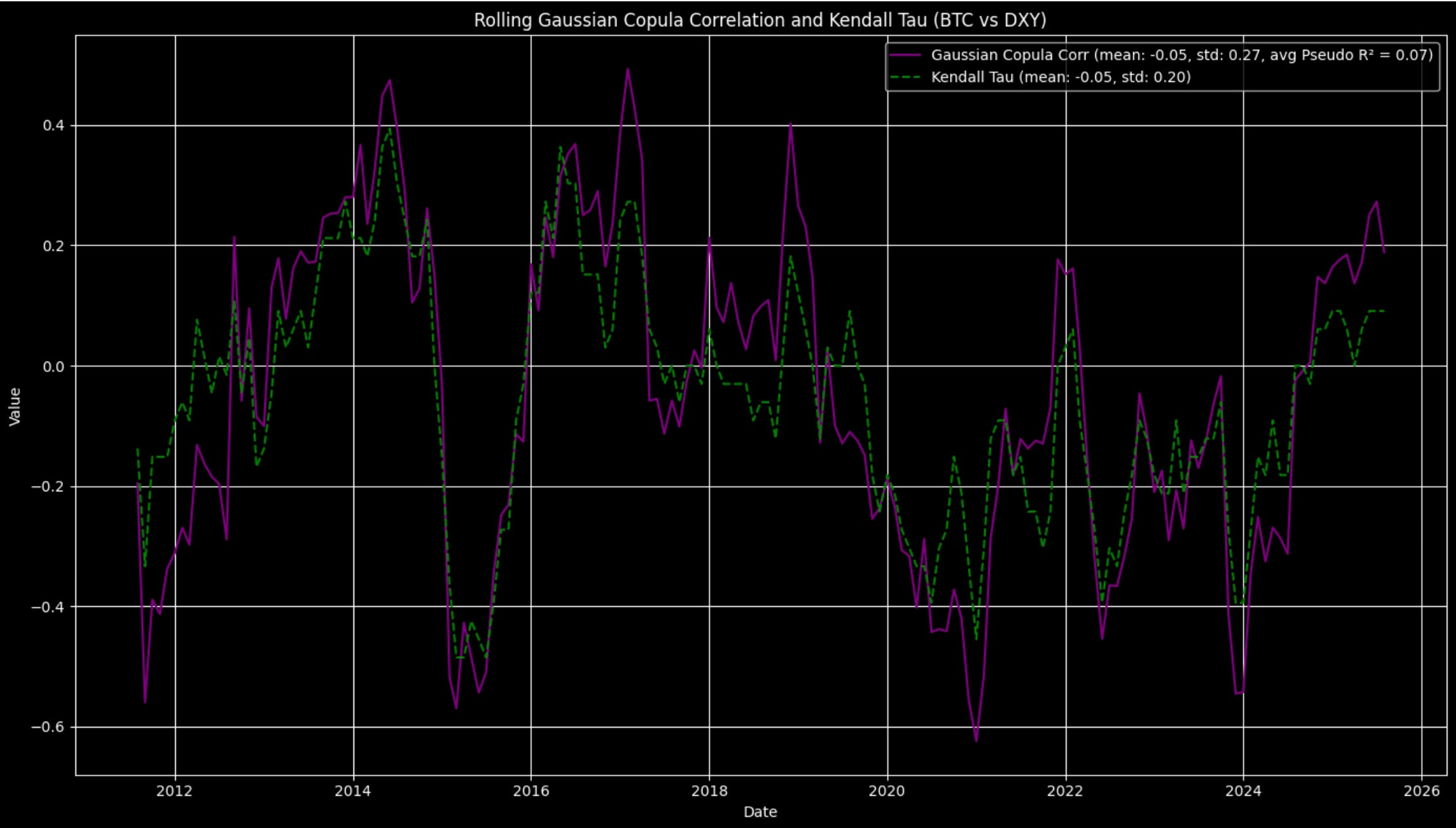

Copula Models

Speaking of tail risk, I decided to implement Copula Models to measure BTC’s tail dependence with SPY, Gold, and the USD Index. I’ve used Copulas for risk analysis before, where I assigned default probabilities. However I thought I’d improvise a tad by implementing Copula models in a dependence analysis–with emphasis on joint distributions.

SPY-BTC’s Copula of 0.29 communicates weak-to-moderate dependence (a stronger value would be closer to 1). Pseudo R-squared of 0.16, conveys weak rank dependence, and Kendall Tau of 0.24, conveys weak concordance, suggesting co-movements are very much noise-driven. As illustrated by the diagram, relationships oscillate–they often bound; however, dislocations are just as prominent, suggesting noise-based coincidences.

The BTC-Gold relationship paints a similar picture, including a very weak Pseudo R-Squared of 0.10, Copula of 0.05, and Kendall’s Tau of 0.04. Again, relationships fluctuate abruptly. However, as an average, we see weak interlinkages.

Finally, BTC-DXY shows a similar relationship with Copula at -0.05, conveying an uncorrelated relationship. In addition, Pseudo R-Squared and Kendall’s Tau are negative-to-negligible.

3) Qualitative Input & Conclusion

You may have noticed that Bitcoin’s correlations tend to spike at certain times. Simply put, this usually reflects systematic investor behaviour—periods when capital turns risk-on, or when risk-off panic drives a flight to cash, prompting simultaneous sell-offs in stocks, Bitcoin, and even gold. Systematic behaviour can result in herding, creating the illusion of meaningful relationships. But given their inconsistency, it’s reasonable to conclude that claims of persistent beta pairings or structural codependence are largely unfounded.

In closing, I’d suggest that factor exploration remains essential before engaging in any forecasting models. Consider examining variables such as network usage, search trends, money supply, bank regulations, and central bank policy shifts—for educational purposes.

4) Links To My Model & Academic Studies Mentioned In Section 1

5) Very Important: Disclaimer

This analysis is provided for informational and research purposes only. It does not constitute financial advice and should not be relied upon as such. The data and interpretations presented may contain inaccuracies or be subject to revision. This content is intended solely to foster further discussion and inquiry among peers. Always conduct your own due diligence or consult a licensed financial professional before making any investment decisions.

Related Tickers: SPY, QQQ 0.00%↑ TSLA 0.00%↑ NVDA 0.00%↑ BTC, GLD, DXY, IBIT 0.00%↑ .

I have to admit that my knowledge of copula models is limited. I think that you might have used t-copula and it obviously showed weak correlation during tails. Correct me if I am wrong here, but that would mean that decoupling of bitcoin from the S&P 500 when US imposed tarrifs was still something that is somewhat expected knowing the unpredictable nature of bitcoin. Is that right?